Travel Insurance Trends Report: Q1 2026

Written By Steven Benna

Written By Steven Benna

About Our Data

Squaremouth is the nation’s largest travel insurance marketplace, with more than 4.4 million insured customers and 23+ years of market data. The following data reflects real traveler behavior drawn from thousands of travel insurance purchases made through the Squaremouth platform. Unlike other industry reports based on surveys or estimates, our data reflects actual trends from finalized insurance purchases.

This report is not a comprehensive look at the travel insurance industry; it’s a focused collection of observations and key trends from our own sales data.

All data on this page is available for media use. Please credit Squaremouth.com when citing.

Key Travel Insurance Trends in Q1 2026

In the first quarter of 2026, travel spending increased to record levels as consumers faced growing travel uncertainty, yet our internal data shows many are not taking the steps needed to properly protect their trips:

- The average trip cost reached an all-time high, surpassing $7,250 for the first time in Squaremouth’s 23-year history, an increase of more than $250 year-over-year.1

- In the first three months of 2026, demand for Cancel For Any Reason (CFAR) coverage surged by +29%, driven by heightened travel risk due to government shutdowns, extreme weather events, geopolitical unrest, and global military conflicts.2

- Despite this record spending and the surge in CFAR interest, 1 in 3 travelers (34%) skipped on standard cancellation protection, leaving the cost of their trip completely unprotected.3

- Our data shows that large portions of traveler segments are underinsuring themselves, including 35% of cruisers, 67% of senior travelers, and 88% of adventure travelers.4

- 95% of travelers heading to the Middle East did not purchase Non-Medical Evacuation coverage, even with significant unrest and instability impacting major travel hubs.5

- All of these data points further emphasize an overall market shift, whereby travelers are opting for more limited coverage than in previous periods.

Skip Ahead To Topics We Cover

- Traveler Spending Reaches All-Time High

- Travelers Forego Trip Cost Protection

- Demand for CFAR Coverage Reaches an All-Time High

- Many Travelers Underinsure Themselves

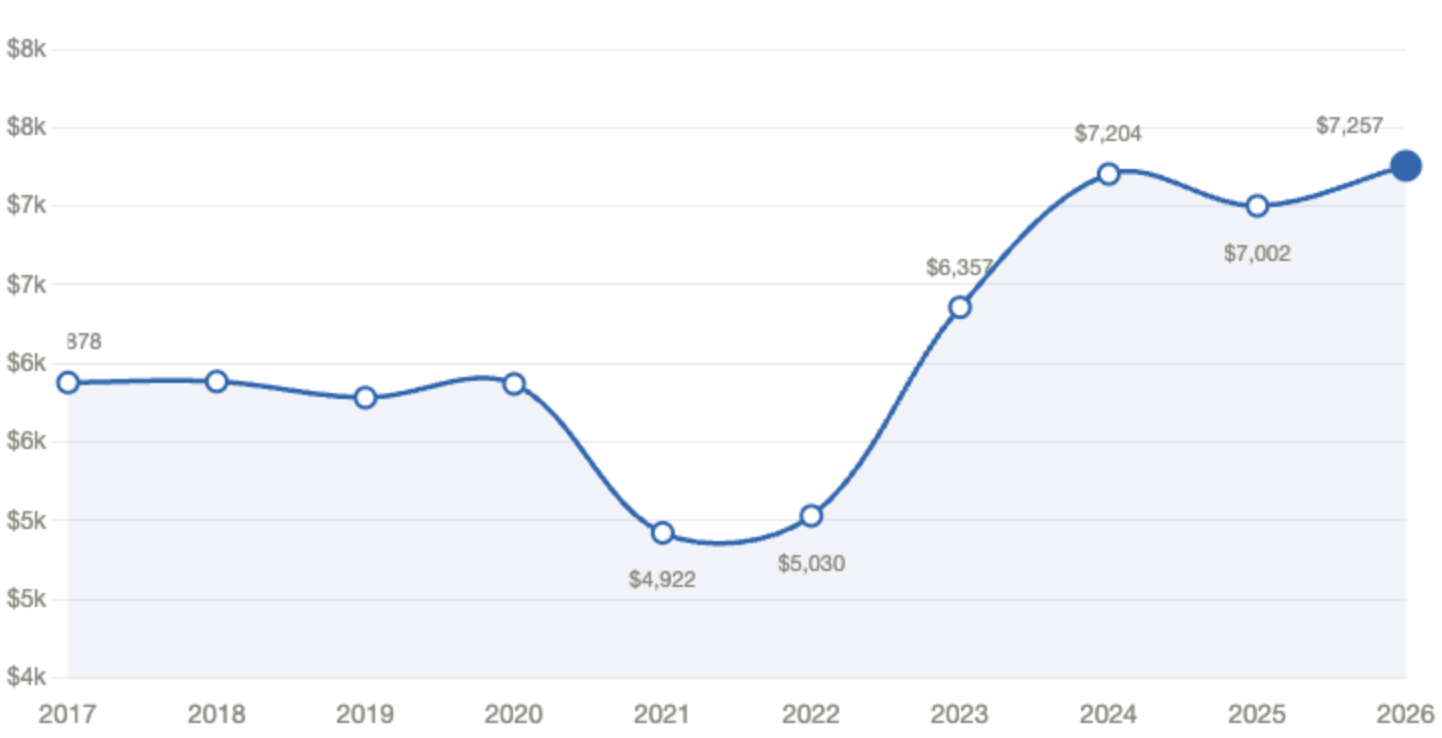

Traveler Spending Reaches All-Time High

- Data from Q1 2026 shows Americans are spending more than ever on travel, with the average trip cost surpassing $7,250, a record high based on historical traveler spending data.

- This marks a 3.6% increase in traveler spending (up $255) versus the same period in 2025.

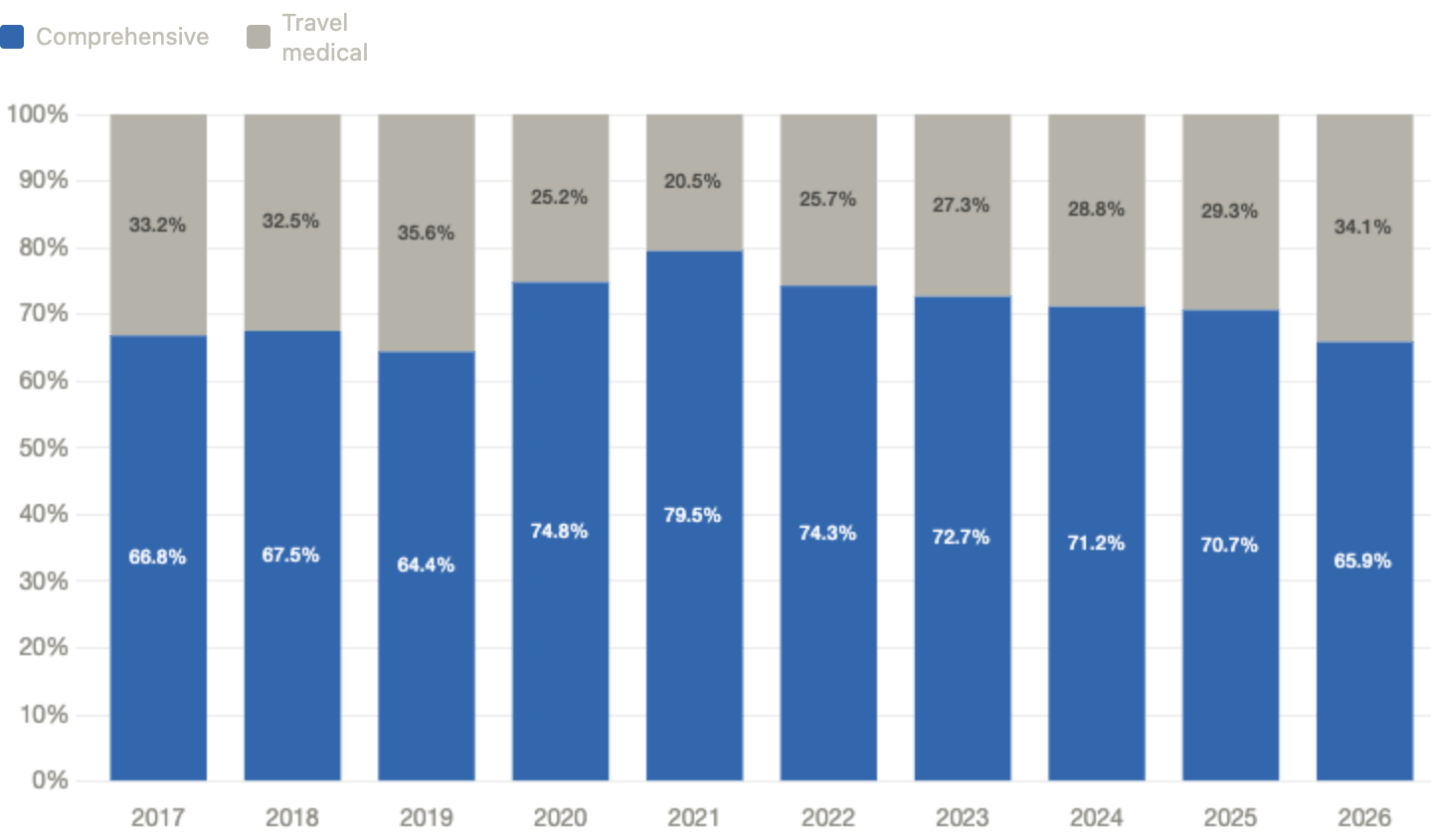

Data reflects the share of purchases by policy type based on actual travel insurance policy sales through Squaremouth.com.

Our internal data shows that this is part of a larger trend witnessed over the past decade, by which average trip costs have grown by +23%. The sharpest acceleration came after Covid-19, when traveler spending surged by +43% in just two years.

Three consecutive years of sustained average cost data point to a new baseline for trip costs, positioning it above $7,000 per trip, with no signs of future declines.

This increase in trip spending among American travelers was brought on by higher airfare due to inflation, global events, and a growing demand for premium travel experiences, such as safari vacations.

These trends have pushed the Travel Price Index up 1.1% year over year.

1 in 3 Travelers Aren’t Protecting Their Trip Costs

- In the first quarter of 2026, more than ⅓ of travelers (34%) purchased medical-only travel insurance and skipped purchasing trip cancellation and interruption reimbursement protection.

- Comprehensive travel insurance sales continued to decline versus recent years, dropping 5 percentage points from Q1 2025.

Data reflects average spending based on actual travel insurance policy sales through Squaremouth.com.

Despite traveler spending being the highest it has ever been, this quarter marked the first time since 2019 that more than 30% of travelers opted out of Trip Cancellation coverage.

The data points to opt-ins for trip cancellation protection returning to pre-COVID numbers. As the Covid-19 pandemic falls further into the past, travelers may be less concerned about trip cancellations than in previous years.

This represents exposure for consumers, as increased travel spending means a greater risk of financial losses.

As part of our expert analysis, we identified three traveler misconceptions that are driving this trend:

- Paying extra for refundable fares instead of opting for trip cancellation insurance

- Believing airline refund rights are enough to cover their whole trip

- Assuming credit cards already provide enough coverage

Below, we look more closely at each of these common missteps, which ultimately put travelers at a greater risk for suffering significant out-of-pocket losses:

Travelers are increasingly booking fully refundable fares, potentially thinking it’s the safest way to prevent out-of-pocket losses related to cancellations. However, refundable bookings often cost more than simply opting for a comprehensive travel insurance plan, which can cost as little as 4% of your trip cost, and leave you unprotected for other common travel disruptions.

Comprehensive trip protection covers all of your prepaid, non-refundable trip expenses (hotels, tours, events, etc.) in a single policy, as well as offering protection for medical emergencies, evacuations, delays, missed connections, and baggage issues.

The US Passenger Bill of Rights, established by the DOT, guarantees travelers refunds for their airfare if a flight is cancelled or significantly delayed, causing some travelers to believe they have enough coverage.

However, it has many gaps that could leave travelers with unexpected out-of-pocket expenses. For example, choosing a refund due to a long delay could mean leaving you stranded and needing to buy expensive same-day alternate arrangements.

Additionally, current airline passenger rights only apply to airfare, leaving hotels, cruises, tours, and other prepaid expenses unprotected.

Comprehensive travel insurance can solve all of these scenarios and more in a single policy.

Travel credit cards offer baseline coverage, but can give travelers false confidence that they have all the coverage they need.

Credit card protection falls short in a few pivotal areas:

- Capped cancellation amounts: Most credit cards cap cancellation coverage at $10,000 per person with a maximum limit of $20,000, while comprehensive travel insurance plans can cover trip costs that exceed $100,000. With these limits, luxury travelers relying on their credit cards are significantly underprotected.

- No Cancel For Any Reason option: We’ve already seen how important this benefit is to travelers. CFAR offers the most possible cancellation flexibility for travelers, which has proven to be crucial in today’s environment. Credit cards do not offer this option to travelers.

- Minimal or no medical benefits: Most credit cards don’t offer any travel medical insurance. Even the best cards only offer $2,500 in coverage, far below the $50,000 that experts recommend. This means that depending only on your credit card’s medical benefits leaves you with a coverage gap of $47,500 or more.

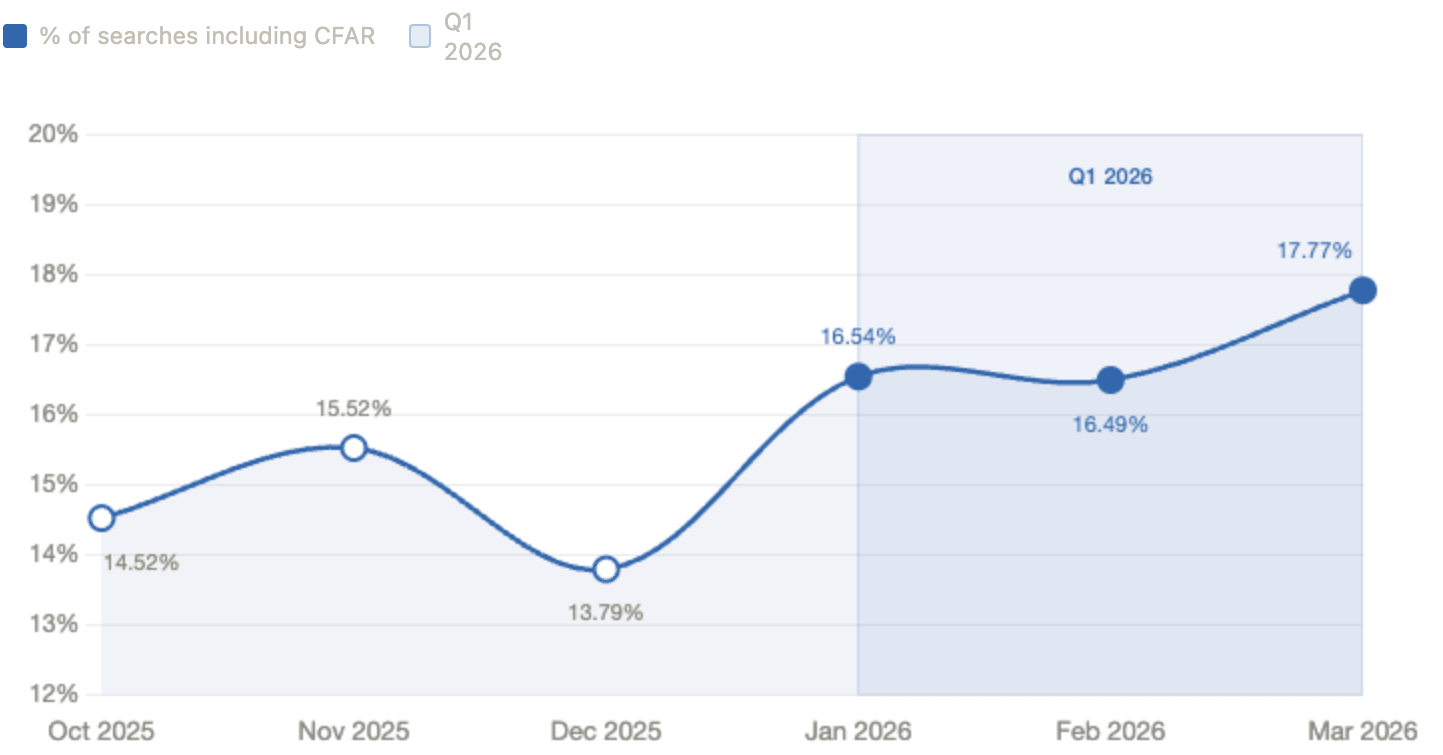

Demand for CFAR Coverage Is at an All-Time High

- In Q1 2026, amid mounting global uncertainty and increased travel disruptions, CFAR became the number one searched benefit among Squaremouth customers.

- Quotes for CFAR coverage overtook quotes for Emergency Medical and Medical Evacuation coverages, which are the two most historically sought-after travel insurance benefits on our platform.

- CFAR searches jumped 29% in Q1, rising from 14% of quotes in December 2025 to 18% in March.

- Despite record interest, 53% of travelers who searched for CFAR still didn’t purchase it. 32% had already missed the time-sensitive window to buy.

Data reflects actual travel insurance searches on Squaremouth.com.

Major world events and travel disruptions caused immediate unease for travelers, driving a surge in demand for CFAR.

At the start of the year, military events in Venezuela and Mexico, and two U.S. government shutdowns, spurred major travel disruptions that were only covered for travelers with CFAR coverage. By January 2026, CFAR quotes had already jumped 20% versus December 2025.

By March, the Iran War had added yet another layer of complexity to global travel, shutting down major hub airports across the Middle East. This spurred another 9% jump in CFAR searches, leading to an aggregate lift of 29% for the quarter.

Yet despite record interest, most travelers who searched for CFAR still didn’t buy it. Only 47% of travelers who searched for Cancel For Any Reason end up purchasing a policy, which could be explained by two factors:

- CFAR is time-sensitive, and is only available for purchase within 10 to 21 days of your initial trip deposit. Our data shows 32% of searchers had already missed that window.

- CFAR typically increases your policy cost by around 40%, which, for travelers already managing rising trip costs, may be a dealbreaker.

However, given the disruptions of Q1 2026, that tradeoff is worth reconsidering.

CFAR protection offers something no standard policy can:

the ability to cancel for reasons an insurer would otherwise deny. Learn more about Cancel For Any Reason insurance

Travelers Are Underinsuring Themselves

- Across multiple traveler segments and demographics in Q1, we saw the same trend repeated: travelers are underinsuring their trips.

- 35% of cruisers bought plans with medical limits below Squaremouth’s recommended thresholds for cruise travel.

- 67% of senior travelers didn’t secure travel insurance early enough to include Pre-Existing Condition coverage within their policy, despite being the most likely group to need this coverage.

- Just 1 in 8 adventure travelers bought plans that cover the specific activities they’ll be partaking in during their trip.

- Only 5% of travelers heading to the Middle East specifically bought a plan with Non-Medical Evacuation coverage, even though this region is facing significant unrest and travel deadlocks.

Over a Third of Cruisers Bought Insufficient Medical Coverage in Q1 2026

![]()

More than ⅓ of cruisers (35%) who buy travel insurance are purchasing plans that do not meet our minimum recommended coverage limits for cruises.

This leaves them responsible for any medical costs that exceed their plan’s coverage limits.

Cruisers have higher medical risks than other travelers due to the complexity of getting treated while at sea. For this reason, they need higher medical coverage than the average traveler. Squaremouth recommends at least $100,000 in Emergency Medical coverage and $250,000 in Medical Evacuation coverage.

Just 33% of Seniors Secured a Pre-Existing Condition Waiver

![]()

More than 66% of senior travelers missed out on securing Pre-Existing Condition coverage when they bought travel insurance, despite being the most likely demographic to have pre-existing medical conditions.

Pre-existing conditions are excluded by travel insurance, unless your plan includes a waiver for these conditions. This waiver is only included if you buy a plan within the time-sensitive window.

Without this coverage, any claim tied to a known condition - whether it’s a cancellation, medical treatment, or an emergency evacuation - might not be covered. Given the risk profile, this mistake can have major financial repercussions. Yet only 33% of seniors meet this deadline.

Travel Insurance Plans with Pre-Existing Condition Coverage

Quote and compare over 100 policies on Squaremouth to find affordable coverage in minutes. Compare Pre-Existing Condition Coverage

Only 1 in 8 Adventure Travelers Got the Activities Coverage They Need

![]()

Heading into 2026, 17% of Squaremouth customers reported they were buying travel insurance for an adventure trip.

However, our data shows that just 2% of travelers overall selected specific activity coverage when buying travel insurance. This means that, on average, only 1 in 8 adventure travelers actually bought the coverage needed for their activities.

Many standard travel insurance plans exclude specific adventurous activities and sports from coverage. If you don’t buy an adventure-specific plan and get injured while participating in an excluded activity, like skiing or hiking, you could nullify your plan’s coverage altogether.

Only 5% of Travelers to the Middle East Bought Non-Medical Evacuation

![]()

The military events in Iran disrupted several of the world’s largest travel hubs in the Middle East and brought major travel uncertainty to the region, impacting destinations like Dubai, Qatar, and Abu Dhabi.

For travelers visiting this region, Non-Medical Evacuation is a key benefit, as it can evacuate you out of a dangerous location during a period of unrest. Just 32% of plans available on Squaremouth’s platform include Non-Medical Evacuation coverage.

Even though most plans do not offer this coverage and the heightened risk of traveling in the Middle East, only 1 in 20 travelers visiting the region specifically bought a plan with this benefit.

Media Inquiries: For questions about this data, interview requests, or custom data pulls, please contact us at: media@squaremouth.com

Citations: Please credit Squaremouth.com when publishing any data from this page. No permission required.